- Published on

How can banks tokenize deposits?

- Authors

- Name

- AbnAsia.org

- @steven_n_t

It's surprisingly simple. Here's how it works 👇

The first thing to understand is that the deposit doesn’t go anywhere.

When you “tokenize” the deposit, it still sits there as a balance in the bank’s system of record.

That means from an accounting (ALM) perspective a bank could still lend against it, sweep it, do whatever it is they do with their balance sheet.

The tokenized deposit becomes its twin.

The token creation then looks very similar to how tokens get created / destroyed for stablecoins through a process called minting and burning.

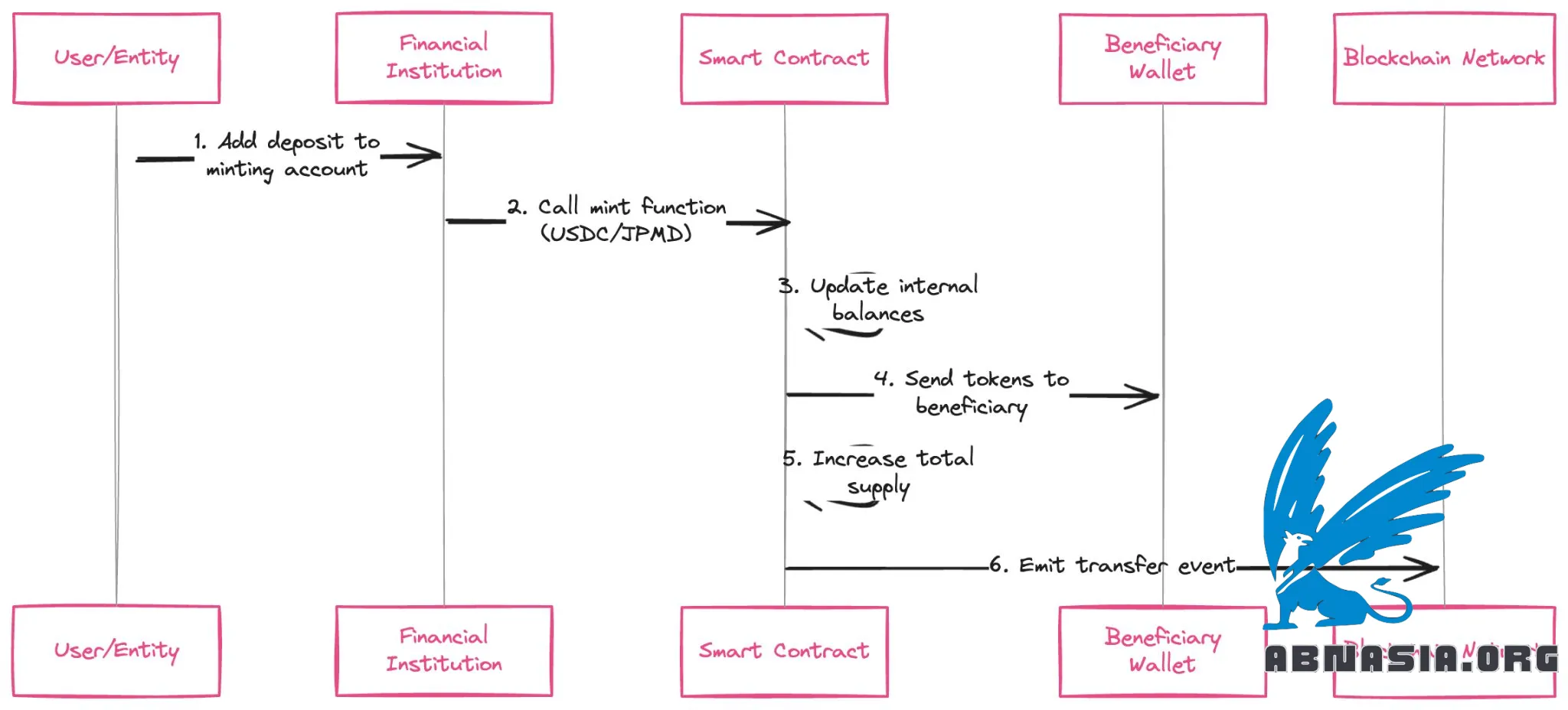

Minting

A deposit is added to a minting account at a financial institution or stablecoin issuer

A token in then minted using the smart contract’s mint function (e.g. USDC, or JPMD)

That token is sent to the wallet address of the beneficiary and the contract updates the internal balances

The total supply of the token is increased by a corresponding amount

A transfer event is sent to the blockchain network to signal this has happened

Burning is a similar process in reverse

A token burn function is called by the smart contract with a specified amount to burn

The burn function reduces the senders balance by a specified amount from their wallet

The total supply of tokens is updated (reduced) and internal balances is updated

The transfer and burn event is sent to the blockchain network to signal this has happened

The deposit is debited from the minting account and credited to the beneficiary

The hard bit is the KYC/privacy tradeoff onchain.

The crypto industry solved KYC in a few ways

- Centralized exchanges and wallets KYC their customers

- They use services like Note Bene to ensure travel rule compliance if a transaction goes above $1,000

- They use blockchain specific transaction monitoring tools like Elliptic or TRM Labs.

For privacy, there are three well-known (not mutually exclusive) paths

Build their own L2s (like a VPN) where they can see the privacy / KYC tradeoffs, and then allow users to swap their deposit token and bridge to another network.

Their deposit token smart contracts can restrict which wallets get to use the token to known, KYC’d entities.

They can use Zero Knowledge Proofs or other privacy-preserving cryptography to not reveal sensitive PII or data.

What right to win do banks have?

Brand power: People know and trust banks to be where their paycheck lands, or for large corporates with managing critical finance functions.

Segments: High-income consumers, large corporates, etc, often prefer the banks.

Distribution (network effects): Banks have millions of customers and deep relationships.

--

You don’t move $2 trillion onto a new technology without thinking it through first.

Author

Ai Base Network (ABN), ABN ASIA was founded by people with deep roots in academia, with work experience in the US, Holland, Hungary, Japan, South Korea, Singapore, and Vietnam. ABN Asia is where academia and technology meet opportunity. With our cutting-edge solutions and competent software development services, we're helping businesses level up and take on the global scene. Our commitment: Faster. Better. More reliable. In most cases: Cheaper as well.

Feel free to reach out to us whenever you require IT services, digital consulting, off-the-shelf software solutions, or if you'd like to send us requests for proposals (RFPs). You can contact us at [email protected]. We're ready to assist you with all your technology needs.

© ABN ASIA